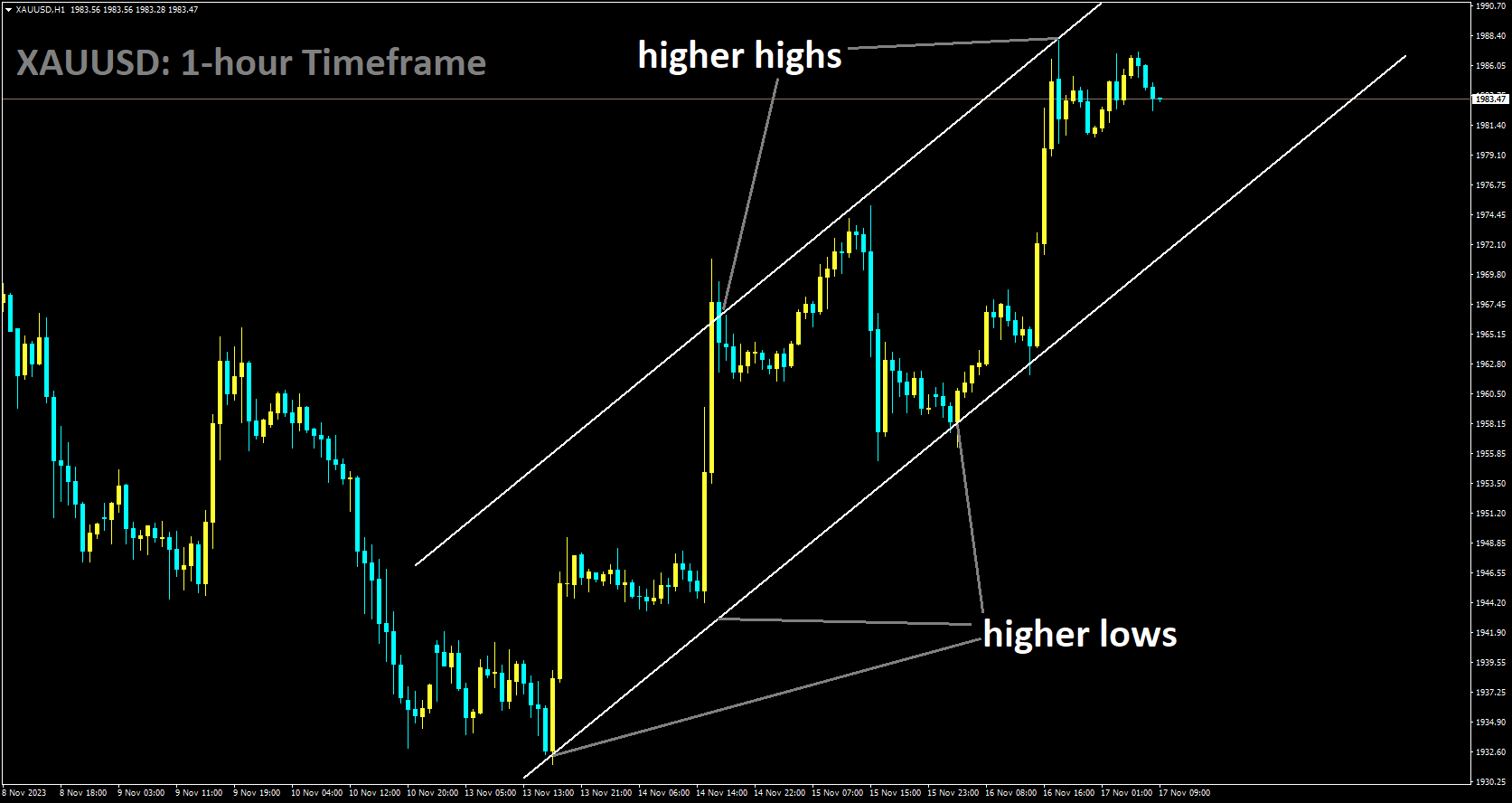

GOLD Analysis:

XAUUSD is moving in Ascending channel and market has fallen from the higher high area of the channel

Gold prices have climbed for the second consecutive day on Friday, marking the fourth positive movement in the last five days. Currently positioned just below a nearly two-week high reached the day before, this upward momentum is attributed to the growing belief in an extended pause by the Federal Reserve (Fed). Softer US macro data supports this sentiment, influencing a surge in the non-yielding precious metal. Furthermore, market expectations for potential interest rate cuts in the first half of 2024 have led to a decline in US Treasury bond yields, putting pressure on the US Dollar. The USD Index, tracking the Greenback against a basket of currencies, struggles to recover from its lowest level since September 1, following subdued US consumer inflation figures earlier in the week.

Mixed signals from high-level US-China talks are also contributing to the appeal of gold as a safe-haven asset, reinforcing the likelihood of further short-term appreciation. Despite this positive trend, XAUUSD is set to register weekly gains of almost 2.5%, snapping a two-week losing streak that saw it reach its lowest level since October 18 on Monday.

Gold has rebounded by over $50 from a multi-week low, touching the $1,932-1,931 range on Monday. This rebound is fueled by the perception that the Federal Reserve has concluded its interest rate hikes. The US Consumer Price Index report earlier in the week indicated a faster-than-expected cooling of consumer inflation, while Thursday’s US Jobless Claims suggested a cooling labor market. Several influential Fed officials acknowledge progress in curbing inflation, reinforcing the idea that the tightening campaign may be nearing its end. Traders increasingly believe that US interest rates will not rise further, with the CME Group’s FedWatch Tool indicating a growing likelihood of the first rate cut by March 2024. The decline in oil prices is also anticipated to have a disinflationary impact, potentially softening the Fed’s hawkish stance and further supporting the price of gold.

International relations between the US and China have seen a slight improvement as military channels are set to reopen, but tension arises from President Biden’s characterization of President Xi as a “dictator.” Traders are now focusing on US housing market data and a scheduled speech by Chicago Fed President Austan Goolsbee for potential short-term opportunities on the last trading day of the week.

SILVER Analysis:

XAGUSD is moving in a Descending channel and the market has broke the lower high area of the channel

The US Dollar (USD) continues to face downward pressure as market participants increasingly bet on the Federal Reserve (Fed) adopting a less aggressive stance. This sentiment is fueled by weak Jobless Claims and Industrial Production figures from the United States, indicating a potential economic slowdown. The US economy’s signs of a slowdown, characterized by a weakening labor market and a retreat in inflation, make it highly improbable for the Fed to raise interest rates at the upcoming December meeting. However, the Fed will closely monitor additional Consumer Price Index and Nonfarm Payrolls reports before making final decisions for 2023, potentially influencing whether a rate hike is eventually considered. The US Dollar Index, recovering from a low of approximately 103.98, has reached 104.30 but remains at its lowest level since September.

In the week ending November 11, US Initial Jobless Claims rose to 231,000, surpassing the anticipated 220,000. The Philadelphia Fed Manufacturing Index showed a slight improvement, reaching -5.9, contrary to the expected -9 points. Industrial Production in the United States fell short of expectations, experiencing a 0.6% month-over-month decline, exceeding the forecasted -0.3%. It also recorded a year-on-year decrease of 0.7%. US Treasury yields continued their decline, with the 2-year rate rising to 4.86%, while the 5 and 10-year rates increased to 4.43%. According to the CME FedWatch Tool, the probability of a 25-basis-point hike in December is currently zero.

USDCAD Analysis:

USDCAD is moving in a ascending channel and the maket has reached higher low area of the channel

US Initial Claims surged by 231,000, marking the highest level in nearly three months. Continuing Jobless Claims also increased to 1.865 million compared to the previous 1.883 million. Market sentiments suggest that the Federal Reserve has concluded its tightening cycle, with expectations of a potential rate cut in mid-2024. This anticipation may weigh on the US Dollar, capping the upside for the USDCAD pair. On the Canadian front, the Canadian Real Estate Association reported a significant decline in house sales for October, the most substantial drop in 16 months, as elevated borrowing rates deterred potential buyers. The Bank of Canada issued a warning last week, advising businesses and households to prepare for higher borrowing rates compared to previous years. Additionally, the Loonie could receive support from a dip in oil prices, given that Canada is a prominent oil exporter to the US.

Looking ahead, market participants will closely monitor US housing data on Friday, particularly Building Permits and Housing Starts. Projections indicate a potential decrease in Housing Starts from 1.358 million to 1.35 million, while Building Permits are expected to decline from 1.471 million to 1.45 million. Furthermore, Friday will bring the release of the Canadian Industrial Product Price Index and the Raw Materials Price Index, which could provide clear direction for the USDCAD pair.

USDJPY Analysis:

USDJPY is moving in a ascending channel and the market has reached higher low area of the channel

The US Dollar faces challenges in staging a meaningful recovery and remains close to its lowest level since September 1, as Federal Reserve expectations lean towards a dovish stance. Market sentiment increasingly reflects the belief that the Fed is unlikely to raise interest rates again, with the possibility of a rate cut by May 2024 being factored into pricing. This shift in expectations follows the release of softer US consumer inflation figures earlier in the week and Thursday’s data on Weekly Initial Jobless Claims, indicating a cooling labor market. Additionally, the recent decline in crude oil prices is anticipated to have a disinflationary impact, bringing the Fed closer to its 2% target and potentially prompting a softening of its hawkish stance. Consequently, the yield on the benchmark 10-year US government bond reached a nearly two-month low on Thursday, further undermining the USD. Meanwhile, a more cautious risk tone in the market is favoring the safe-haven Japanese Yen and putting some pressure on the USDJPY pair. Despite this, the downside is tempered by the Bank of Japan’s (BoJ) adoption of a more dovish stance.

BoJ Governor Kazuo Ueda reiterated on Friday that the central bank will persist with its ultra-loose monetary policy, emphasizing the need for patience as it is not yet certain that the 2% inflation target will be achieved in a stable and sustainable manner. Ueda acknowledged that it will take time, but inflationary pressures driven by cost-push factors are expected to dissipate, and Japan’s trend inflation should gradually accelerate toward 2% through fiscal 2025. This stance is likely to limit gains for the JPY and discourage traders from making aggressive bearish bets on the USDJPY pair. Looking ahead, market participants are turning their attention to US housing market data, specifically Building Permits and Housing Starts, for potential momentum during the early North American session. Additionally, a scheduled speech by Chicago Fed President Austan Goolsbee and movements in US bond yields will play a role in influencing the dynamics of the USD.

GBPUSD Analysis:

GBPUSD is moving in a ascending channel and the market has fallen from the higher high area of the channel

In October, UK Retail Sales experienced a month-over-month decline of 0.3%, contrary to the anticipated 0.3% growth and the previous month’s registered -1.1%, as per official data from the Office for National Statistics (ONS) released on Friday. Core Retail Sales, which excludes auto motor fuel sales, also dropped by 0.1% month-over-month, deviating from the expected 0.4% increase and the previous month’s -1.3%. The annual Retail Sales in the United Kingdom saw a significant decline of 2.7% in October, surpassing the expected -1.5% and the previous month’s 1.0% drop. Likewise, Core Retail Sales for the same period fell by 2.4%, exceeding the anticipated -1.5% and matching the previous month’s figure.

Specifically, automotive fuel sales volumes fell by 2.0% in October 2023, while over the three months leading to October, sales volumes saw a 0.7% decline compared to the preceding three months, potentially influenced by rising fuel prices. In the same period, food store sales volumes decreased by 0.3%, contrasting with the unchanged (0.0%) figure in September 2023. Non-food store sales volumes also declined by 0.2% in October 2023, following a substantial 2.1% fall in September 2023. Retailers attributed this downturn to factors such as the cost of living, reduced footfall, and adverse weather conditions in the latter half of the month. On a positive note, non-store retailing, predominantly online retailers, experienced a rebound, with sales volumes rising by 0.8% in October 2023 after a decline of 2.4% in September 2023.

Crude Oil Analysis:

Crude Oil is moving in Descending channel and the market has reached the lower low area of the pattern

During the Asian session on Friday, West Texas Intermediate Crude Oil prices exhibited a narrow trading range and consolidated following the overnight decline to a four-month low. The current trading level hovers just above $73.00 per barrel, signaling the potential for a fourth consecutive week of losses. Concerns are mounting with the softer US macroeconomic data, amplifying worries about a more pronounced global economic slowdown that could impact fuel demand and continue to weaken Crude Oil prices. In October, US monthly Retail Sales experienced their first decline in seven months, signaling a slowdown in demand as the fourth quarter begins. Additionally, the number of initial unemployment insurance claims in the US rose to 231,000 for the week ending November 11, up from 218,000 in the previous week.

These factors compound existing anxieties about a deceleration in China, the world’s leading oil importer, and diminishing concerns about potential supply disruptions from the Middle East. These factors collectively reinforce a negative outlook for crude oil. Furthermore, the prevailing belief that the Federal Reserve has concluded its policy-tightening measures, with potential rate cuts in the first half of 2024, keeps US Dollar bulls on the defensive. Despite a subdued USD price action, there is minimal encouragement for bullish traders or support for oil prices. The lack of buyer interest and an absence of a substantial recovery in oil prices indicate that the bearish trend may still be ongoing. However, with technical indicators on the daily chart approaching oversold territory, it may be prudent to await near-term consolidation or a modest rebound before anticipating the next move. Nevertheless, oil prices appear set to record losses exceeding 5% for the week.

CADJPY Analysis:

CADJPY is moving in Ascending channel and market has reached higher low area of the channel

In the recent hour, Deputy Finance Minister of Japan, Ryosei Akazawa, emphasized the government’s commitment to intervening in the foreign exchange market to prevent excessive volatility. He clarified that there is no predetermined FX level that would trigger intervention, and any such actions would be specifically targeted at curbing excessive market fluctuations. Akazawa made it clear that intervention would not be prompted solely by the weakening of the Japanese Yen. The primary objective of any intervention would be to address and stabilize overall market volatility.

GBPJPY Analysis:

GBPJPY is moving in Descending channel and market has reached lower low area of the channel

Traders are currently awaiting the release of UK Retail Sales figures for a potential market catalyst. Meanwhile, the recent release of softer UK consumer inflation data on Wednesday has reinforced the belief in the market that the Bank of England will initiate rate cuts in the near future. This perception is identified as a significant factor contributing to the British Pound’s comparatively weak performance and putting pressure on the GBPJPY cross. Additionally, a subdued risk sentiment is prompting some safe-haven flows toward the Japanese Yen JPY, contributing to a slightly bearish tone.

Despite the overall appreciation of the JPY, a definitive upward move remains elusive, partly due to the Bank of Japan’s adoption of a more dovish stance. BoJ Governor Kazuo Ueda reiterated on Friday the central bank’s commitment to maintaining ultra-loose monetary policy settings, citing the elusive sight of sustained achievement of the inflation target. Ueda expressed the expectation that trend inflation would gradually accelerate toward 2% through fiscal 2025. Furthermore, Japan’s Deputy Finance Minister Ryosei Akazawa echoed the commitment to stability, stating that the government stands ready to intervene in the foreign exchange market to curb excess volatility.

Despite the overall appreciation of the JPY, a definitive upward move remains elusive, partly due to the Bank of Japan’s adoption of a more dovish stance. BoJ Governor Kazuo Ueda reiterated on Friday the central bank’s commitment to maintaining ultra-loose monetary policy settings, citing the elusive sight of sustained achievement of the inflation target. Ueda expressed the expectation that trend inflation would gradually accelerate toward 2% through fiscal 2025. Furthermore, Japan’s Deputy Finance Minister Ryosei Akazawa echoed the commitment to stability, stating that the government stands ready to intervene in the foreign exchange market to curb excess volatility.

AUDUSD Analysis:

AUDUSD is moving in Box pattern and the market has reached resistance area of the pattern

The Australian Dollar faces continued challenges and sustains losses, despite the unfavorable economic data released from the United States on Thursday. The weakness in the AUDUSD pair may be attributed to a prevailing risk-off sentiment, possibly influenced by the Federal Reserve’s uncertain stance on the trajectory of interest rates. However, the subdued conditions in the US labor market, coupled with recent inflation data, contribute to the prevailing belief that the Fed is unlikely to pursue further interest rate hikes.

Despite positive developments such as an upbeat Australian jobs report and heightened inflation expectations, the Australian Dollar failed to capitalize on these factors. The seasonally adjusted Employment Change for October exceeded market expectations significantly. However, a notable portion of the added jobs were in the form of part-time positions, diminishing the overall positive impact on the headline figure. The US Dollar Index is displaying a sideways movement with a negative bias, following a session characterized by volatility that ultimately favored the Greenback. Despite weak economic data and declining US bond yields, the US Dollar managed to recover ground, with the yield on the 10-year Treasury note reaching a low of 4.43% on Thursday.

Notably, US Continuing Jobless Claims for the week ending on November 3 reached their highest level since 2022, standing at 1.865 million compared to the previous reading of 1.833 million. Additionally, Initial Jobless Claims for the week ending on November 10 rose to 231,000 against the expected 220,000, marking the highest level in nearly three months. However, there was a positive note in the form of the Philadelphia Fed Manufacturing Survey, which reported a figure of -5.9, indicating an improvement compared to the previous -9.0 print. Looking ahead, the forthcoming US housing data on Friday is anticipated to offer fresh insights into the housing sector, potentially influencing trading decisions in pairs like AUDUSD.

NZDUSD Analysis:

NZDUSD is moving in a ascending channel and the market has fallen from the higher high area of the channel

The New Zealand Dollar faces challenges as concerns about China’s property sector outweigh the positive impact of Wednesday’s Retail Sales and Industrial Production data. Given New Zealand’s significant role as a major exporter of dairy products to China, the Kiwi is particularly sensitive to developments in the Chinese economy. October’s Fixed Asset Investment in China increased by 2.9%, falling below the expected 3.1% and disappointing in terms of consistency. However, the Chinese government’s injection of 1 trillion Yuan in low-cost financing for the property sector is seen as a strategic measure to address concerns about a potential credit crunch. This move could have global economic ripple effects, affecting the New Zealand Dollar.

Despite a significant improvement in New Zealand’s Producer Price Index Output for the third quarter, rising from 0.2% to 0.8%, the NZD seems to lack substantial support. On the other hand, the US Dollar is displaying a sideways trend amid positive jobless claims data. Despite challenging labor market conditions, with US Continuing Jobless Claims reaching their highest level since 2022 and Initial Jobless Claims rising to the highest level in almost three months, these factors seem insufficient to weaken the USD’s resilience. Continuing Jobless Claims for the week ending November 3 increased to 1.865 million, compared to the previous reading of 1.833 million. Initial Jobless Claims for the week ending November 10 rose to 231,000, exceeding the expected 220,000. Looking ahead, the upcoming US housing data on Friday is expected to provide fresh insights into the housing sector, potentially influencing trading decisions in pairs like NZDUSD.

Despite a significant improvement in New Zealand’s Producer Price Index Output for the third quarter, rising from 0.2% to 0.8%, the NZD seems to lack substantial support. On the other hand, the US Dollar is displaying a sideways trend amid positive jobless claims data. Despite challenging labor market conditions, with US Continuing Jobless Claims reaching their highest level since 2022 and Initial Jobless Claims rising to the highest level in almost three months, these factors seem insufficient to weaken the USD’s resilience. Continuing Jobless Claims for the week ending November 3 increased to 1.865 million, compared to the previous reading of 1.833 million. Initial Jobless Claims for the week ending November 10 rose to 231,000, exceeding the expected 220,000. Looking ahead, the upcoming US housing data on Friday is expected to provide fresh insights into the housing sector, potentially influencing trading decisions in pairs like NZDUSD.

🔥Stop trying to catch all movements in the market, trade only at the best confirmation trade setups

🎁 60% FLAT OFFER for Signals 😍 GOING TO END – Get now: forexfib.com/discount/